Currency Exchange Rate Update…

The Pound continues to outperform its major peers.

It remains at the very top end of the trading range of the last 11-months against the Euro. It is trading at a 15 month high against the US Dollar; a 17 month high against the Canadian Dollar and recently touched its highest level against the Aussie Dollar since May 2020.

What’s In The News?

In The UK…

The upward momentum of the Pound is being driven by diverging interest rate expectations. The financial markets believe that unlike the Fed and others, the Bank of England (BoE) will continue to raise UK interest rates. The UK-US two-year bond yield spread climbed last week to hit its highest level since 2014.

UK macro-economic data out last week confirmed that wages continue to rise at the joint highest rate on record. Whilst the UK economy shrank by less than expected in May.

The UK government has confirmed public sector workers will receive at least 6% pay increases. This follows the worst period of industrial unrest since the 1990’s.

All of these developments continue to reinforce the idea that the BoE is likely to continue to raise UK interest rates to tackle inflation. In the short term, that will support the Pound as funds flood into the UK from overseas investors. Beyond that thelonger-term economic drag from all these interest rate increases; the looming housing crisis and credit risks should all weigh on the pound’s attractiveness further down the line.

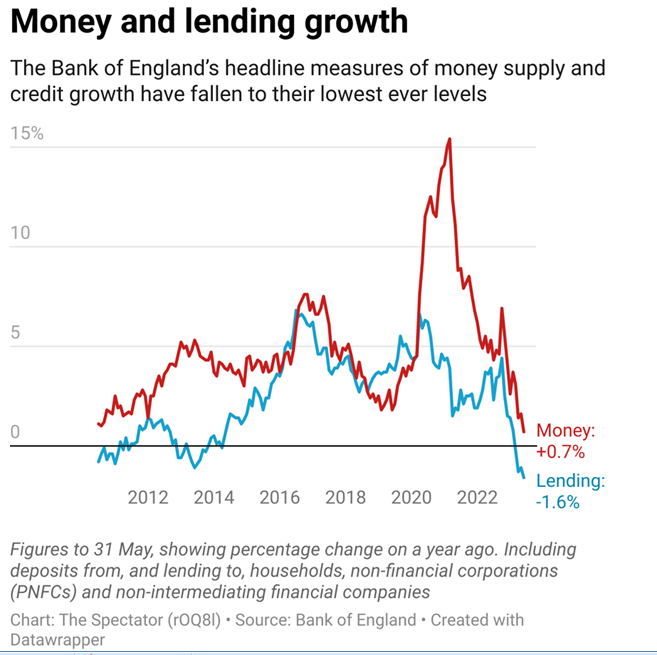

The BoE’s quarterly credit conditions survey, lenders reported “losses and default rates on secured loans to households increased in Q2 and were expected to increase in Q3”.

Lenders reported that the availability of secured credit, the vast majority of which is mortgages decreased in the previous three months and was expected to fall further over the next three months.

Consultants TwentyCi reported that the number of homes available for rent in the UK has plunged to a 14-year low. Amid an exodus of landlords from the market. With just 241,000 private rental properties available in June compared to 370,000 the same month four years ago. A drop of 35%.

UK private landlords have been hard hit by rising buy-to-let mortgage rates; the threat of more red tape regulation and the loss of tax breaks, prompting many to sell up.

TwentyCi said “Rental availability had reached its lowest level since its records began in 2009”.

The Office for National Statistics (ONS) reported 128,000 working days were lost in May due to industrial action relative to the 257,000 lost in April.

Accountants PwC reported that over-55s who left their jobs during the pandemic in the UK are the least likely to return to work in any of the G7 countries. A “Great Retirement” during Covid-19 has left Britain with a quarter of a million more 55 to 64 years old’s who are economically inactive, neither in work nor looking for work. The trend has left the UK economy struggling with 1 million vacancies and still below its pre-Covid size.

In The EU…

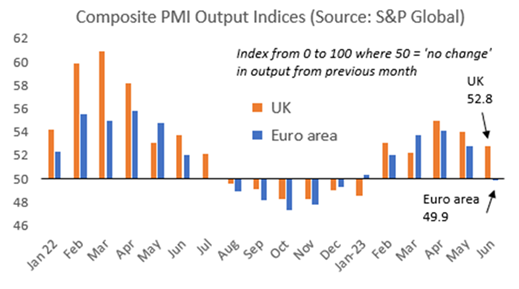

One of the few forward-looking economic indicators we have is the PMI, the Purchasing Managers Index.

Whilst the rise of the value of the Pound against the Dollar does hint at Dollar weakness as much as pound strength, the rise in the value of the Pound against the euro seems to be more stable with the UK consistently outperforming the Euro area economy across all economic sectors.

In The USA…

The US dollar index has slumped to a fresh 15 month low. Softer than expected US producer and consumer price data out last week continues to support speculation that the Federal Reserve (FED) may have come to the end of its interest rate raising cycle.

The annual consumer inflation rate in the US slowed to 3% in June, its lowest level since March 2021.

The dollar index is now down over 12% from its September 2022 peak. The fall of the Dollar has accelerated recently with every G10 currency strengthening against the USD over the past month.

Other…

China’s exports recorded their biggest decline in more than 3 years last week, plunging by 12.4% from a year ago. Imports declined by 6.8% over the same period, also worse than expected.

Zhiwei Zhang, president and chief economist at Pinpoint Asset Management said “Latest data in the developed countries show consistent signals of further weakness. Which will likely put more pressure on China’s exports in the rest of the year. China has to depend on domestic demand. The big question in the next few months is whether domestic demand can rebound without much stimulus from the government.”

China’s annual producer prices sank for a ninth month in a row in June. While consumer prices remain unchanged as the Chinese economy tethers on the verge of deflation.

The Drewry index of world container shipping collapsed by 86% from its peak in September 2021. It is currently 45% below its 10 year average.

THE COSMOS OFFER

Of course, currency market volatility can bring trouble but with careful monitoring can also bring opportunity.

At Cosmos, we provide our clients with a relationship not a transaction-based service.

We are pro-active not reactive.

We offer local collection accounts in: the USA; Canada; the EU and the UK saving clients time and money on transfers.

Cosmos Currency Exchange has won multiple awards for its customer service and pro-active approach.

Please call +44 (0) 300 124 6409 or email us to discuss your individual currency requirements.

Quote

This week’s quote comes from the great Abraham Lincoln

“The best way to predict your future is to create it”.